In today’s financial markets there is misinformation pertaining to Bank Guarantee and Standby Letter of Credit transactions, largely due to the lack of correct information available. In order to keep informed one must go out of their way to learn about the industry and how it operates. The Bank Instrument industry is a world where real information, truthful processes and real bank instrument providers are hard to come by. Here we will try to provide some useful information so that you can educate yourself further on how this industry operates. In this section we will talk about Standby Letters of Credit.

What Is A StandBy Letter Of Credit? Letters of Credit (LC) can be classified as either documentary Letters of Credit or Stand By Letters of Credit (SBLC/SLOC). A Documentary Letter of Credit allows payment to the seller. It facilitates the movement of goods in an international transaction. In trade finance, Letters of Credit is one method of payment used to reduce risk in global transactions between a Buyer and Seller of goods. They are mainly used for commodity and industrial use as performance bonds. A Standby Letter of Credit is an agreement, not intended to be drawn upon but is a safeguard in the event of non payment by either party mentioned in the contract. You can either lease or purchase a Standby Letter of Credit. In other words; an SBLC is a document issued by the bank guaranteeing payment on behalf of their client. The bank confirms the collateral is held within their clients account, the client buys an instrument and it is then freshly cut backed by Providers capital. De possible to Monetize an SBLC.

Finance A Business Using An SBLC Standby Letters Of Credit can be used to finance a business; particularly those looking to grow or expand. Having a SBLC monetized is the best and quickest way for a business to get some much needed cash. Bank instruments can be monetised and used to enter into trade platforms. SBLC’s could be one of the best alternative ways to finance a business. Reason being is that you are not dependent on a lender per se. It is likely that the funds will arrive in tranches and this could be a perfect way to manage your capital.

What Parts Do Banks Play In SBLC Transactions? Technically speaking, “Banks DON’T issue Standby Letters of Credit” Instead, the bank is the deliverer not the initiator of the transaction, they CONFIRM their client has the sufficient funds. For example; let’s pretend you use a courier to deliver a parcel to a customer. You are the Provider of the parcel and the courier is the delivery agent who delivers your parcel to the Receiver. The courier isn’t the Provider of the parcel, they are just the delivery agent whom the Provider uses to send the parcel from the Providers location to the Receivers location. using the above example, banks operate exactly the same way when handling Standby Letters of Credit. The bank acts as the courier and they receive a financial instruction from a Provider to deliver one of the Providers assets (Bank Guarantee — BG or SBLC) to the Receiver’s bank. In other words, the banks are in place of the courier, being that they are the Sender and Receiver of SWIFT message (Whether it be MT760, MT799..etc..)

Genuine SBLC Providers

As discussed at the beginning, genuine SBLC Providers can be hard to come by. The banks don’t advertise SBLC’s as their own bank products, simply because they are not allowed to. Standby Letters of Credit are provided by high net worth clients with large cash holdings in an account at the Bank. High net worth clients are usually hedge funds, private equity, pension funds, and large coprations etc.. It is very difficult not only to get in touch with bank instrument Providers, they are very strict too, they don’t mess around. Genuine Providers perform many checks and balances which means that any authorised mandate agents connected to Providers are too follow strict procedures. This is good new on our part as we know we carry clean business but it means that any business we introduce needs to be able to follow certain procedures. Because of the strict ruling, HubHolzer will let you know what is required but in general we will ask for POF and BCL to say you can pay for 10% of the LTV/face value of the bank instrument. We want to know that every business that passes us has the capability to afford the lease fee.

How Do SBLC’s Work?

When a company completes the forms to lease an SBLC, what they are essentially doing is borrowing collateral (what this is actually called is a temporary “CTA” Collateral Transfer Agreement). Let’s say that you are an oil refinery company looking to buy oil and are dealing with say ABC Oil. You have an agreement with ABC Oil saying that you want to buy $100M USD worth of oil (on your books you have $103 1-JSD) . You may choose not to use your own bank account and apply through your own bank but instead, prefer to lease a StandBy Letter Of Credit from a different Provider. There are several ways SBLC’s can be used and it is all in the wording of the MT760. Providers can issue Standby Letters Of Credit for the purposes of:

- Trade and commerce — (for purchasing of goods).

- They can also be used to back credit lines issued by banks.

- And/or project funding.

As well, there are Providers who can issue cash backed SBLC’s which are monetizable. However we will need to know who the monetiser is in order to assign the SBLC in favour of the Monetizer.

SBLC Document Application and Requirements

When leasing a bank instrument, the DOA is a legal agreement signed by both Parties. It states that the titled owner will lease the SBLC for one year and one day at $100M USD giving it back with no liens or encumbrance. The legal documents is called a Deed of Agreement (DOA). Both banks will also send a Ready Willing and Able (RWA) message to each other. The Providers bank confirms it’s ready to issue the SBLC and Receivers bank confirrns their client has the funds. After the DOA and RWA are signed and SWIFT fees are paid, the banks of both parties will message each other until the instrument is transmitted to the Receiver. In some agreements should one fail to meet the timeline, there will be a penalty and risk of no further business. Two things to take note: 1) There is no standard leasing process, leasing programs differ and each determined by the Provider. 2) The Provider instructs the bank what to do therefore if you choose to go through a ba lots of paperwork as they have policies and guidelines to ahere to.

Lease An SBLC

You can apply to lease an SBLC in one of two ways. One way is to apply for a StandBy Letter Of Credit with your bank or; use authorized agents such as ourselves and fill in a DOA (deed of Agreement). Some terms and timelines may be negotiated (there may be an element of flexibility through some Providers). We stress that buyers should clearly understand the documents before signing them. Double check your details, be clear and correct as it can be a very costly mistake. The Providers bank will send a Ready, Willing and Able Letter on behalf of of their client. It’ll say something like ” Our client on behalf of [bank] is RWA”…. the receiving bank also sends a RWA on behalf of the Receiver. The SWIFT fees are then called upon and the SWIFT messages are exchanged bank to bank until SBLC is issued. A hard copy of the SBLC will be sent to the Beneficiary.

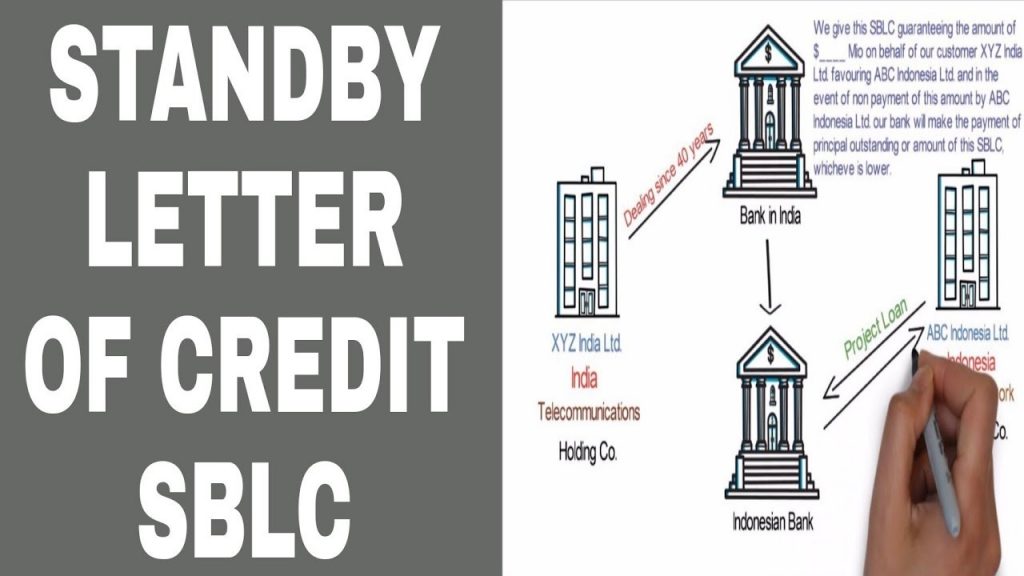

SBLC Funding Process

The image below is an example of the process of acquiring the bank instruments for a Standby Letter of Credit. When the banks have completed their messaging, you may receive a hard copy of the SBLC/MT760. Just bear in mind whether its for commerce purposes or if you can have the SBLC monetized. This is the part many people often get confused.

Fresh Cut SBLC

Fresh Cut only means that it has been freshly issued, “seasoned instrument” means that it was issued in the past and is in the secondary market. People buy fresh cut bank instruments as the bank instrument comes from a direct credible source thus knowing exactly the person/organisation who cut the instrument for lease. Usually bank instruments such as SBLC’s are time limited and should be paid back in full to the Provider within the time specified.

Monetizing An SBLC

After leasing an SBLC, you may want to monetise it. All that happens when you monetize an SBLC is the instrument is converted into legal tender. This can take up to IS days to process and verify. Your bank should be able to do this for you. It wont be monetised for the full amount as it can vary on a number of factors such as; bank rating, country of issuance, LTV etc.. The instruments must be in your name and there is a time limit on a leased SBLC’s. These bank instruments can only be leased for one year and one day. Bank instruments are checked for forgery and there are strict guidelines to adhere to. Heavy due diligence will be undertaken. Banks that issue fresh cut bank instruments must be UCP-600 compliant and be a top banking institution.

Purchasing A Standby Letter Of Credit

Purchasing an SBLC, it is similar to the process of leasing a StandBy Letter Of Credit. The main difference is that you own the instrument in your company [name. For example: The Provider iS the asset owner, asset holder and asset controller. If you choose to purchase the SBLC, the title of goods will be transferred to you. Purchasing an SBLC is advantageous in that you can then choose to lease the instrument out if you so choose to do so. Ask us about our low cost SBLC’s that can be put into a managed trade platform.

SBLC Project Financing V’s Conventional Funding

Conventional funding can take a long period of time from submission to receiving funds for a project. The reasons can include;

- A lengthy due diligence procedure and/or

- Whether or not the funder has an appetite

- Other projects in the pipeline thus having to wait a few months.

Financing projects with an SBLC can be a cheaper and faster route as the procedure takes a few weeks and is less onerous. Leasing a bank instrument can be also a cheaper as some investment banks charge thousand of dollars to fund a project. Please note; it is our requirement that we ask you to provide Proof of Funds and/or a bank comfort letter. This is to demonstrate to the Provider that the companies we represent are in good faith and in trust to pay leas fees.

Swift Fees

When people apply for an Standby Letter of Credit most do not understand how the mechanism behind the transaction works. There are certain buyers who think that there are no fees involved when issuing a bank instrument and presume the SWIFT messaging service is free. This is not the case. The banks of both parties communicate as per the DOA agreement using SWIFT messages, recognizable to us as MT messages. Please check on the search engines for (Link to another website with typical SWIFT Fees SWIFT charges). Sending a SWIFT message isn’t cheap, these are banks charges! We suggest that if you need an SBLC, prepare at least 12% of the asking amount to go towards the cost of an SBLC. One way in which the buyer might not have to pay SWIFT Fees is by having the bank issue a Bank Comfort Letter (BCL). This letter just sates that the Buyer has the funds. This needs to be arranged before the DOA is signed.

Other Fees:

Depending on the Provider we generate our fee from the cost of the instrument. You may notice a purchase/lease price plus a commission price eg (10+2). The commissions are paid for any intermediaries/brokers. We keep our commissions low to Provide you with a fair deal. Need A Large Bank Instrument?

If you need a Stand By Letter Of Credit for a substantial amount (ie in the Billions in tranches), we can arrange this for you on a case by case basis.

Information About SBLC Procedures

Please note that it is NOT advisable to change the SBLC Procedure writte are not in a position to dictate to our Providers how to operate their Proc able to give you a few choices on different Providers. Changing procedur frowned upon as it makes the validity of the SBLC enquiry questionable. We have partnered with a firm to provide trade and commerce letters of forward transactions. please let us know your requirements on the conta

How To Apply For A Bank Instrument

You can apply to have an Standby Letter Of Credit either through a bank services. We can give you a number of low cost options to help fund you team has streamlined the process the paper work saving time and heade you through the process from start to finish.